Print PDF

Self insurer licensing framework review discussion paper

1. Introduction

The State Insurance Regulatory Authority (SIRA) regularly reviews its regulatory frameworks to ensure requirements remain risk-based and focused on achieving customer and system outcomes.

This discussion paper will seek views on the existing self-insurer licensing framework. SIRA will consider all feedback received during the consultation process and will ensure that changes to the self-insurer licensing framework are tailored to the current risk, regulatory, and economic conditions.

The closing date for submissions is 17 September 2021 1 October 2021

2. Purpose

The purpose of this discussion paper is to seek views of stakeholders on opportunities to update the self-insurer licensing framework by:

- aligning with the licensing frameworks of other SIRA regulated insurers;

- applying the SIRA Customer Service Conduct Principles;

- considering the Independent Pricing and Regulatory Tribunal’s (IPART) A best practice approach to designing and reviewing licensing schemes – Guidance material; and

- taking into consideration the outcomes of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

SIRA is seeking feedback on existing arrangements to determine:

- whether the current framework is fit for purpose; and

- where regulatory arrangements can be tailored to account for and address risks to achieving the objectives of the scheme.

We invite you to tell us your views by using our online form or emailing us directly, following your consideration of the questions posed in this paper. Further information about how to make a submission can be found on page 11 of this discussion paper.

SIRA will consider your response, reasoning and evidence for any change in determining licence conditions and changes to the framework.

3. Objectives

- Review the licensing application process and licensing conditions of self-insurers to improve outcomes for customers and the workers compensation system.

- Align licence conditions of self and specialised insurers and Home Building and Compulsory Third Party insurers where possible.

- Establish conditions to mitigate insurer risks for self-insurers.

- Ensure the procedure for licence cancellation is documented and effectively finalises all claims and policies of insurance.

4. Background

Self-insurance was originally introduced in NSW to allow an individual employer to accept the responsibility of providing workers compensation insurance for their own workers if they could provide adequate security in the context of a privately underwritten scheme. In order for the employer to obtain a licence they were required to meet the liabilities when called upon to do so. (Hansard, 12 January 1926).

Section 210 of the Workers Compensation Act 1987 (1987 Act) states that an employer may apply for a self-insurer licence. A company may also apply for a licence if the licence is intended to cover wholly owned subsidiaries that are employers.

Section 211 of the 1987 Act states the Authority may consider the following matters when considering an application for a self-insurer licence:

(a) the suitability of the applicant;

(b) the financial ability of the applicant to undertake the liabilities under this Act;

(c) the efficiency of the workers compensation system generally; and

(d) such other matters as the Authority thinks fit.

The licensing framework is structured to facilitate the achievement of the workers compensation system objectives through the supervision of self-insurer performance in the areas of conduct and claims management (together representing suitability), and financial ability.

SIRA has taken steps to strengthen its regulatory approach more generally since the 2015 legislative reforms which allowed for the development of Licensed Insurer Business Plan Guidelines. SIRA has also issued Standards of Practice under section 192A of the 1987 Act which established SIRA’s overarching principles and requirements for insurers’ management of claims to improve claimants’ experience, outcomes and support.

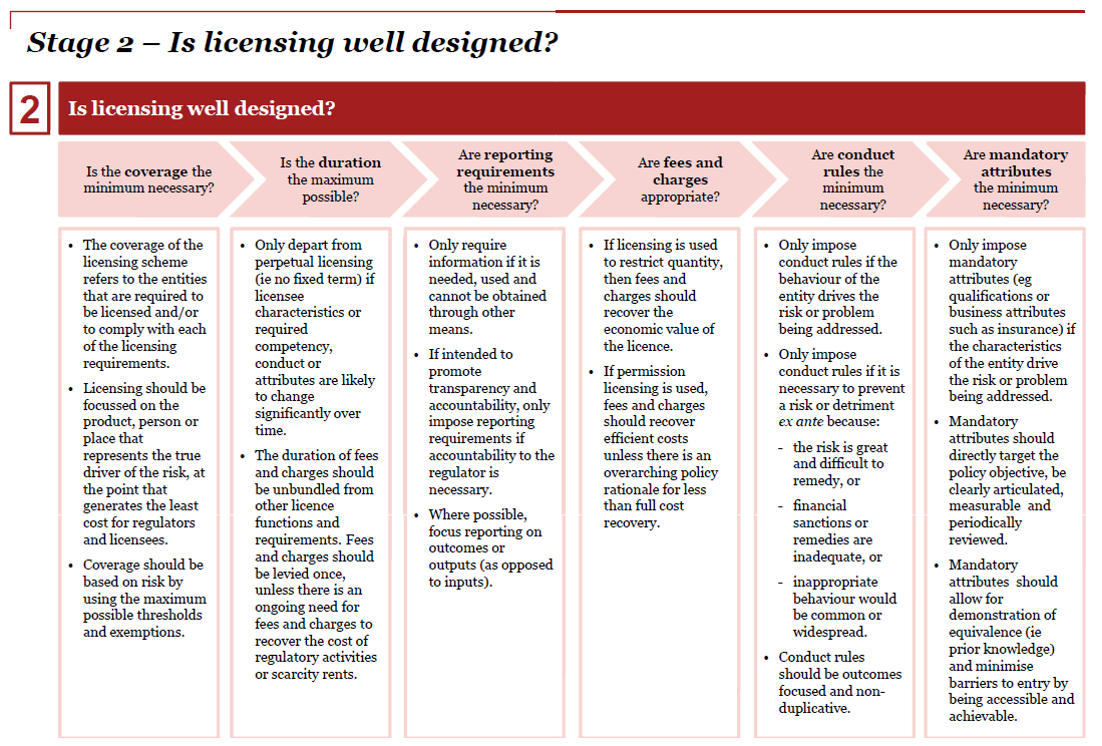

IPART: Review of licensing schemes

The Best practice approach to reviewing and designing licensing schemes commissioned by the IPART in 2013 was developed based on best practice principles. It is intended to be applied as an assessment tool to both existing and proposed licensing schemes. The review of the self-insurer licensing framework will employ the IPART framework as the foundation of the proposed licensing requirements.

The IPART framework considers whether:

- licensing is an appropriate activity;

- the licensing framework is well designed;

- the licensing process is administered effectively and efficiently; and

- the licensing scheme is the best response.

Licensing is considered appropriate if:

- there is an ongoing need for action;

- nothing else addresses the problem;

- there is an ongoing need for a regulatory response; and

- licensing is still required to address the policy objectives.

This paper focuses on the design of the licensing framework (see table below).

5. Current state

Self-insurer licence applicants must first meet certain requirements to ensure they are able to conduct themselves in accordance with the legislation, are financially viable and can maintain high standards of injury management and case management throughout the term of the licence. In recent years there has been a growing interest in self-insurance and an increasing trend in outsourcing of insurance related functions which makes this review timely to ensure the framework remains appropriate in this changing market dynamic.

A self-insurer licence establishes additional operational conditions that supplement legislative requirements. In order for SIRA to achieve the workers compensation system objectives outlined in the Workplace Injury Management and Workers Compensation Act 1998 (1998 Act), SIRA expects self-insurers to:

- comply with legislation; and

- comply with licence conditions by performing to SIRA standards in the areas of:

- conduct (incorporating legislative compliance and regulatory reporting);

- claims management; and

- financial ability.

Self-insurers must comply with the legislative requirements and licence conditions to maintain continuity of their licence.

The performance of self-insurers is currently measured against the Self-Insurer Tiering Model. The model adopts a risk based approach to determine the measures that inform tiering classifications for self-insurers. SIRA regularly monitors self-insurer performance against the tier measures for conduct, claims management and financial ability. Self-insurers receive regular feedback from SIRA in relation to their performance against these standards. This tiered supervisory model acknowledges exemplary and acceptable workers compensation performance. It also detects risks to the achievement of workers compensation system objectives, prompting a risk-based regulatory response from SIRA.

6. Review of licensing arrangements

6.1 Licence application

Division 5, part 7 of the 1987 Act contains the licensing provisions of self-insurers. Sections 210 and 211 of the 1987 Act refer to the application for and determination of self-insurer licences.

Section 210 of the 1987 Act provides that an employer may apply for a self-insurer licence. A company may also apply for a licence if the licence is intended to cover wholly-owned subsidiaries that are employers. An employer may make the application to SIRA directly or may engage a broker to act on their behalf.

Section 211(2) states that SIRA may take the following matters into consideration in determining an application for (or renewal of) a licence:

(a) the suitability (such as the conduct and claims management capability) of the applicant; (b) the financial ability of the applicant to undertake the liabilities under this Act;

(c) the efficiency of the workers compensation system generally, and

(d) other matters as SIRA thinks fit.

Currently, a prospective self-insurer must provide the following information as part of their application:

- applicant information;

- workers compensation information;

- claims management information;

- financial information;

- completed and signed declaration; and

- additional information to support the application.

Preferred outcomes

- The application process aligns with legislative intent.

- The business making the application is financially viable and motivated by more than cost savings alone.

- The business making the application is engaged, accountable and is available and able to respond to queries and requests for information as part of the application process, whether or not a broker is engaged to support the application.

- The business making the application can demonstrate sound governance of itself and any outsourced providers.

- The applicant is able to demonstrate competent case management capability.

- Granting a licence is likely to result in improved scheme efficiency through competition, best practice and innovation

Questions

- Are the current application requirements fit for purpose?

- If an external advisor is engaged to assist the potential applicant, how can SIRA ensure that an applicant will retain or develop sufficient internal expertise to manage its responsibilities as a self-insurer?

- Should SIRA define expectations and requirements about the suitability of the applicant in other dimensions in addition to conduct, structure, system, finances, people, experience?

- How can SIRA ensure that applicants can demonstrate capability in resourcing and expertise to carry out the workers compensation business?

- Should SIRA require comprehensive premium and claims information from the current insurer to determine whether self-insurance is a better option?

- Should a cost benefit analysis be required to assist in determining whether an employer should become self-insured?

- What due diligence and governance systems should an applicant demonstrate if they are choosing to outsource claims handling or other functions?

- How should SIRA assess whether outsourced arrangements will meet requirements and result in preferred outcomes?

- If claims handling is to be managed internally by an applicant, what is the best method to measure internal capability and governance?

- Should the new applicant provide evidence of:

- a learning and development program for workers compensation staff;

- a quality assurance program;

- a case management model;

and provide ongoing reporting as part of their business plan?

- How should a new applicant best demonstrate the change in culture and sound governance required in the move from being a policy holder to a self-insurer?

- Should the requirement for a minimum number of employees for a new applicant be reviewed?

- Is there a different approach to financial modelling that would work better in assessing an applicant’s position?

- Are there any other matters SIRA should consider?

6.2 Financial viability

Section 182 (1) (c) enables SIRA to set conditions in relation to security for the purpose of securing the insurer’s liabilities under the Act. SIRA currently imposes security requirements on self-insurers in line with its security policy.

Preferred outcomes

- SIRA must ensure that all of an insurer’s liabilities are able to be paid in full in the event of insolvency.

- Competitive neutrality concerns are addressed i.e. that any actual or potential self-insurer can compete on even ground with the NSW Government’s Nominal Insurer.

Questions

- What is the best way for SIRA to assure that all claims liabilities are funded by the insurer in the event of insolvency?

- Does the way SIRA hold security for self-insurers need to be reviewed? What are the suggested alternatives?

- Should there be a review of the calculation methodology by which the security is determined?

- Are there any other matters SIRA should consider?

6.3 Work health and safety

A principal objective of SIRA under section 22 of the 1998 Act is to promote the prevention of injuries and diseases at the workplace and the development of healthy and safe workplaces. To facilitate this, SIRA’s current licensing framework requires that a self-insurer must perform its workplace obligations and functions as an employer in accordance with the requirements of the Work Health and Safety Act 2011.

Work health and safety (WHS) is important for a self-insurer as it bears both the organisational and financial risk arising from its workplace practices. By proactively managing workplace safety risks and caring for employees, a self-insurer may improve its overall workers compensation outcomes and facilitate the achievement of workers compensation system objectives. SafeWork NSW is responsible for administering the work, health and safety legislation. SafeWork NSW will report the workplace conduct and legislative compliance of each self-insurer to SIRA for assessment of licence conduct.

Preferred outcomes

- To promote the prevention of injury and illness in the workplace.

- To promote innovation within insurers in assisting employers to prevent work related injury.

Questions

- What is the best way for a self-insurer to influence WHS outcomes for their overall business?

- How should the self-insurer demonstrate that injury management and WHS claims management staff share knowledge about WHS requirements and processes?

- Are there any other matters SIRA should consider?

6.4 Conduct

Since its inception, SIRA has introduced expectations in relation to insurer conduct. These include:

- Standards of practice; and

- Customer service conduct principles

These are in addition to Standard condition 3.1 which states The Licensee must conduct itself as a licensed self-insurer in accordance with the legislation and provide acceptable reporting to the Authority. This includes business planning, workplace safety and claims information.

While the expectation for an insurer to meet these conduct requirements has been made clear, greater detail in the self-insurer licence conditions is important to ensure an insurer’s understanding and adherence to the expectations outlined.

Preferred outcomes:

- Insurers achieve compliance with the legislation and conduct themselves in a manner which provides system participants with positive experiences and outcomes.

- Insurer conduct is in line with community and regulator expectations.

- Once a self-insurer is licensed, ongoing exemplary conduct is demonstrated throughout the duration of the licence.

Questions:

- How best can SIRA ensure self-insurers adhere to conduct expectations?

- Should further detail regarding conduct expectations be outlined in the licence conditions?

- How and when should self-insurers articulate to SIRA the values and behaviours of their organisation which underpin their conduct?

- How should self-insurers demonstrate adherence to the customer service principles?

- Are there any other matters SIRA should consider?

6.5 Culture and Governance

There is currently no licence condition that requires a self-insurer’s board or senior executives to collectively have a good understanding of workers compensation insurance and for this to be demonstrated. A new licence condition would seek to ensure a self-insurer’s board /senior executive group is competent to provide effective governance and oversight of the licence and workers compensation performance.

Preferred outcomes:

- Insurer has robust governance framework in place, providing oversight and understanding of workers compensation outcomes and performance.

- Insurer can demonstrate sound prudential management.

- The board / senior executive group fosters a culture of compliance and risk management.

- Insurer is professional, responsive and transparent in its engagement with the Regulator.

Questions

- How should SIRA ensure that a self-insurer’s board or senior executive is able to demonstrate a required level of expertise and skill in workers compensation and that their workers compensation insurance business is conducted in line with the objectives of the legislation?

- Should employee satisfaction surveys, cultural reviews/reporting information be included in the self-insurer business plans submitted to SIRA or reported in another way?

- How should an insurer demonstrate that the culture and governance of outsourced service providers aligns with the self-insurer’s culture and governance and the expectations of the regulator?

- Are there other ways to achieve, demonstrate and assess better outcomes / governance?

- Are there any other matters SIRA should consider?

6.6 Claims Handling

Currently SIRA requires that an insurer must perform its obligations and functions as a licensed self-insurer in accordance with the legislation and demonstrate performance in injury and claims management of a standard acceptable to the Authority.

When a function is outsourced to a third-party the self-insurer, as the licensed entity, remains accountable for the performance of outsourced parties and any instances of non-compliance. Before outsourcing the whole or any part of any key operational functions the licensee must notify SIRA in advance.

Preferred outcomes

- Ensure appropriate accountability and understanding of their obligations by the licensed entity.

- Ensure appropriate capability and capacity of the functions of the insurer to achieve good outcomes for system stakeholders.

Questions

- Should this licence condition be strengthened to define expectations?

- How can SIRA best ensure that self-insurers have appropriate resourcing with sufficient knowledge and experience to perform their obligations in claims management?

- How should SIRA require that insurers demonstrate that they have the necessary infrastructure, systems, processes and resources to perform their obligations and functions (including injury, claims and complaints management) as a licensed insurer in accordance with legislative requirements and to the commercial standards acceptable to SIRA?

- How can SIRA best ensure that self-insurers maintain appropriate oversight of outsourced arrangements, given their continued accountability?

- When should SIRA be provided with copies of service level agreements, reporting or monitoring, models that reflect performance of the outsourced provider? Should evidence of any penalties imposed by the self-insurer on their outsourced provider for poor performance also be provided to SIRA?

- Should self-insurers have to demonstrate exemplary conduct and claims handling practices for a minimum period after their self-insurance licence is granted before they can apply to purchase their tail liabilities?

- Should SIRA’s approval be required for outsourcing arrangements?

- Are there any other matters SIRA should consider?

6.7 Licence duration

Currently, SIRA may grant self-insurer licences for a term of up to eight years. Licences continue to be in force until the expiration of the licence term, their renewal or the suspension or cancellation of the licence by SIRA. Section 183 of the 1987 Act outlines the arrangements for the cancellation or suspension of licences.Self-insurers apply for renewal in accordance with the process outlined in the Self-insurer information requirements.

Under section 180 of the 1987 Act, SIRA also has discretion to grant licences for shorter terms if it deems such action is warranted either at the time of issuing the first licence, or on renewal of a licence.

For new applicants, SIRA will grant a self-insurer licence for a period up to three years and work with the new insurer to help them meet their requirements.

Some stakeholders have expressed concern that the current licence term arrangements may create business uncertainty.

IPART recommends perpetual licensing with the intent of minimising the administrative burden on the licensee and the regulator.

Preferred outcomes

- The licence term reflects the ongoing nature of claim liabilities.

- The licence term takes into account SIRA’s enhanced supervision activities as an oversight mechanism that replaces some of the historical functions of five-yearly licence renewal.

- The licensee is authorised to hold a self-insurer licence without restrictions providing they meet their legislative and regulatory obligations

Questions

- What are the benefits or risks if SIRA was to introduce an indefinite licence period?

- If an indefinite licence term were to be considered, what licensing restrictions would be appropriate in the case where specific performance risks / issues were identified?

- If an indefinite licence term were to be considered, and SIRA formed the view that the self-insurer was no longer complying with their legislative and regulatory obligations, what should the process be to give notice to cancel or suspend the self-insurer licence?

- If an indefinite licence term is not the best option, how should the licence term be determined? What should the maximum term be?

- Are there other matters for SIRA to consider?

6.8 Any other comments?

Is there anything that SIRA can implement in its licensing framework to drive better return to work outcomes for self-insured employers and their workers?

How to make a submission

SIRA invites individuals and organisations to contribute to share their views, experiences and insights on the self-insurer licensing framework.

The consultation questions in this paper are not intended to be exhaustive, but rather are provided to assist with focusing feedback on key considerations. While SIRA encourages stakeholders to address the consultation questions within their submission, this is not a requirement and all feedback will be considered.

You are encouraged to attach any evidence that will support your views and provide specific examples where possible.

Your submission can be lodged via:

- the SIRA website www.sira.nsw.gov.au

- email to [email protected]

The closing date for submissions is 17 September 2021 1 October 2021.

Submissions to this consultation may be published on the SIRA website. If you do not wish to have your submission published, please state this clearly on your submission.