Print PDF

CTP Scheme quarterly report - June 2017

Introduction and summary

The New South Wales Compulsory Third Party (CTP) Scheme is governed by the Motor Accidents Compensation Act 1999 (the Act). The Green Slip market currently comprises six licensed insurers operated by four entities: Suncorp (AAMI and GIO), Allianz Australia (Allianz and CIC Allianz), NRMA and QBE. The market is split into two segments: retail and non-retail. AAMI, GIO, Allianz and NRMA compete mainly in the retail segment, CIC Allianz competes in the non-retail commercial vehicle market and QBE operates in both market segments.

Section 172 of the Act requires SIRA to inform each licenced insurer of their premium market share on a quarterly basis. Additionally, SIRA provides detailed average Green Slip price trends and claims reports to insurers every quarter. The claims trends include aggregate claims numbers and claims costs, illustrating the claims experience of the current scheme.

During the June 2017 quarter, no insurer implemented new prices. GIO continued to offer the best price of $606 for Sydney passenger vehicles. Despite NRMA’s best price being $34 above GIO, NRMA dominated the market with a share of around 31 per cent due to its brand impact, branch network and product bundling.

All insurers lodged premium filings with SIRA during the June 2017 quarter which SIRA approved to take effect from 1 July 2017 (September 2017 quarter). Initially all insurers except one filed for varying price increases of up to $40 but SIRA’s final assessment resulted in individual price reductions of up to $43.

A further round of premium rate filings will be required for policies to be issued from 1 December 2017, taking into account the changes introduced in the Motor Accident Injuries Act 2017. It is expected that most policyholders will receive reductions in their Green Slip prices from 1 December 2017 as a result of the CTP reform.

Green Slip premiums and market trends

Insurer premium filings

Insurers set their own Green Slip premiums in a competitive market, within part 2.3 of the Act and the Motor Accidents Premiums Determination Guidelines approved by the SIRA Board. Insurers can file proposed premiums with SIRA at any time and there is no limit to the number of filings an insurer may lodge each year.

SIRA may only reject a premium filing if it is of the opinion that the premium:

- will not fully fund the present and likely future liability of the insurer

- is excessive having regard to actuarial advice and to other relevant financial information

- does not conform to the Motor Accidents Premiums Determination Guidelines (PDG).

The scheme actuary, Ernst and Young, and SIRA internal analysts review the assumptions underpinning each premium filing. The assumptions include projected industry and insurer’s claims costs, economic factors, expenses, profit loading and insurer’s forecast market share.

Adjustments to the Medical Care and Injury Services

(MCIS) levy

The MCIS levy is made up of a Motor Accidents Fund (MAF) levy and Lifetime Care and Support (LTCS) levy. SIRA Board is able to review and adjust the MAF component of the MCIS Levy as required under s.213 and s.214 of the Act. SIRA sets the levy in order to generate a balanced budget outcome, while maintaining a preferred prudential reserve target.

The LTCS levy component could also be adjusted by the Insurance and Care NSW (iCare) Board of Directors to meet the Board’s target funding amount for a specified period.

There was no change to the MCIS levy rates during the June 2017 quarter.

Headline prices

Table 1: Sydney car headline price changes

Filing period | NRMA | GIO | AAMI | Allianz | QBE | CICA |

|---|---|---|---|---|---|---|

June 2017 quarter ($) | 640 | 606 | 622 | 623 | 613 | 673 |

March 2017 quarter ($) | 640 | 606 | 622 | 623 | 613 | 673 |

December 2016 quarter ($) | 624 | 590 | 603 | 628 | 611 | 662 |

June 2017 quarter price change $ (%) | 0 (0) | 0(0) | 0(0) | 0(0) | 0(0) | 0(0) |

March 2016 quarter price change $ (%) | 16 (2.6) | 16 (2.7) | 19 (3.2) | -5 (-0.8) | 2 (0.3) | 11 (1.7) |

Table 1 shows the changes in headline prices that occurred during this reporting quarter. The headline price is the lowest CTP premium price (including levies and GST) offered by each insurer to a new retail customer, aged 30 to 54, for a private use passenger vehicle garaged in Sydney.

GIO continued to offer the best market price of $606 for a Sydney passenger vehicle during this reporting quarter. Despite NRMA’s best price being $34 above GIO, NRMA continued to dominate the market due to its brand impact, branch network and product bundling.

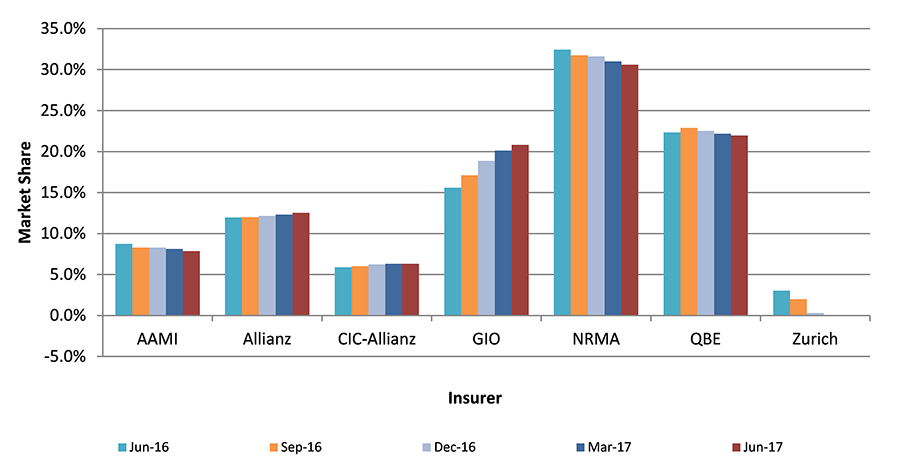

Premium market share

Table 2: Insurer market share in the NSW CTP scheme

| Premium share for individual quarters | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Insurer | 4 quarter average | Jun-17 | Mar-17 | Dec-16 | Sep-16 | Jun-16 | Mar-16 | Dec-15 | Sep-15 | Jun-15 |

| % | ||||||||||

| AAMI | 7.9 | 7.7 | 7.8 | 7.6 | 8.2 | 8.8 | 8.5 | 7.6 | 10.1 | 10.6 |

| Allianz | 12.5 | 13.0 | 13.2 | 12.5 | 11.4 | 12.2 | 12.6 | 11.9 | 11.2 | 12.0 |

| CIC-Allianz | 6.3 | 5.7 | 6.1 | 6.9 | 6.6 | 5.7 | 5.8 | 6.0 | 6.1 | 5.2 |

| GIO | 20.8 | 21.6 | 20.5 | 21.1 | 20.1 | 18.8 | 15.4 | 14.0 | 14.1 | 13.2 |

| NRMA | 30.6 | 30.8 | 30.7 | 30.7 | 30.2 | 32.5 | 33.2 | 31.1 | 32.9 | 34.0 |

| QBE | 22.0 | 21.2 | 21.9 | 21.2 | 23.5 | 22.0 | 32.2 | 22.7 | 21.3 | 21.0 |

| Zurich | -0.1 | 0.0 | 0.0 | 0.0 | 0.0 | 0.0 | 1.3 | 6.7 | 4.2 | 4.1 |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

Insurers are required under the Act to submit information on insurance premiums to SIRA at the end of each quarter. This information is used to determine the premium market share for each insurer and to report trends in premium levels over time.

The total amount of premiums collected (excluding MCIS levy and GST) during the year to 30 June 2017 was $2.65 billion. This represented an increase of around 11.8 per cent on the previous year ($2.37 billion).

Table 2 shows NRMA continues to lose market share year-on-year but still remains the insurer with the largest market share. Its premium market share at the end of the June 2017 reporting quarter was 30.8 per cent, compared to 32.5 per cent the same period last year. GIO gained a significant 2.8 per cent market share compared to the June 2016 quarter.

Allianz and CIC Allianz gained marginal 0.8 per cent and 0.1 per cent market share respectively compared to the June 2016 quarter. NRMA, AAMI and QBE lost 1.7%, 1.1% and 0.8% market share respectively compared to June 2016 quarter.

Graph 1: Premium market share (rolling 12-month) comparison

Graph 1 shows the proportion of premiums collected in the 12 months to the quarter end. Based on rolling twelve month periods this graph reduces any volatility that exists from quarter to quarter due to the seasonal renewal of large fleet vehicles and shows smoother trends in market share.

AAMI, NRMA and QBE market shares continue to decrease, while GIO continued to gain market shares in the last twelve months. Allianz and CIC Allianz market shares have been relatively stable.

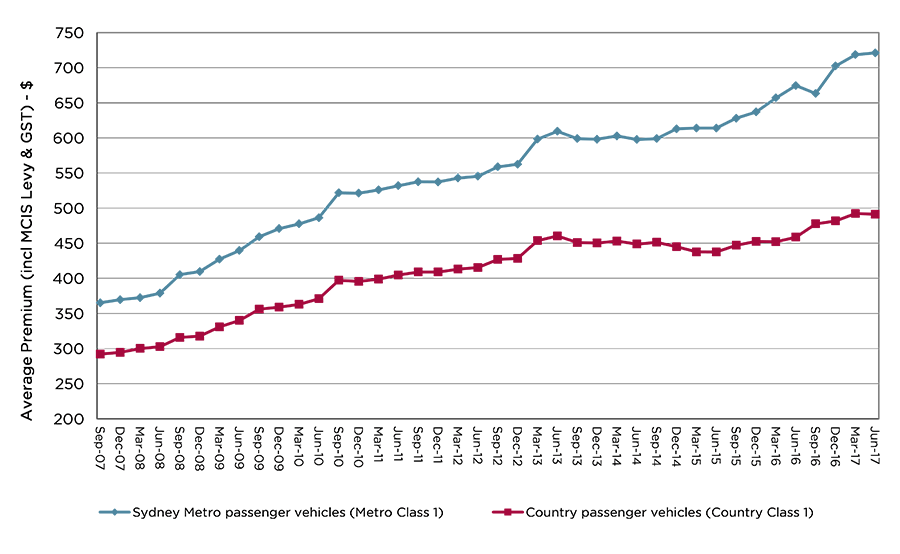

Premium trends

Graph 2: Average premium (quarterly trends)

In the June 2017 quarter (Graph 2):

- The average premium (including MCIS levy and GST) paid by Sydney passenger vehicle owners was $721, an annual increase of $47 (6.9 per cent).

- The average premium paid by Country (regional) passenger vehicle owners was $491, an annual increase of $33 (7.1 per cent).

The observed general upward trend in premiums is mainly due to:

- increasing claims frequency even though it appears to decline in the last four quarters (Graph 5). Insurers factored in the reduction in claims frequency during the past four quarters in their 1 July 2017 premium filings which may result in reduced average premiums from September 2017 quarter

- reduction in bond yields following the Global Financial Crisis to the historically low levels sustained since 2015, resulting in low investment returns (Graph 3); and

- inflationary increases to claim costs such as medical treatment, economic loss calculations and salary-related expenses.

While the increase in the number of small claims reduces the overall average claims cost, the long term increase in claims frequency means the overall effect is an increase in the cost per policy.

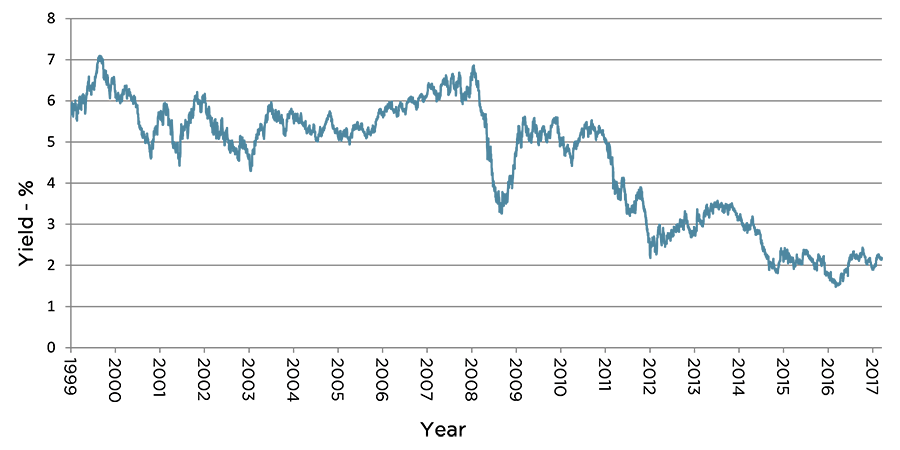

Graph 3: Trend in five year Commonwealth Bond yield to 15 August 2017

Graph 3 shows movements in the five-year Commonwealth Government bond yield since the inception of the current CTP Scheme 17 years ago.

Low bond yields have a negative impact on the investment returns of insurers who invest collected premiums in the bond market. The yield on the five-year Commonwealth Government bond has been at historically low levels in recent years and material changes are not expected in the short term. Movements in five-year bond yields are generally consistent with movements in the yields of other maturities.

Claims trends

Number of claims

Newly reported claims

Claims trends are measured from 5 October 1999, when the current Act (MACA) came into effect. The scheme actuaries complete an annual valuation of the scheme in June each year to provide projections for the number of claims expected to be reported. In the June 2017 quarter, the actual number of newly reported claims since the previous quarter, March 2017, was 4,139. This is 11 per cent less than the 4,633 anticipated from the June 2016 actuarial valuation of the scheme. Some of these newly reported claims were lodged with respect to past accident quarters. However, the number of claims reported from accidents in the latest accident quarter, June 2017, was 2,040, which breaks the trend that started in March 2008. This reduction could be because of a number of factors including: the new Legal Costs regulation; a market response to Strike Force Ravens[1], which was set up in August 2016 to investigate CTP fraud in South Western Sydney; and implementation by insurers of new claims management practices designed to combat fraud and exaggeration.

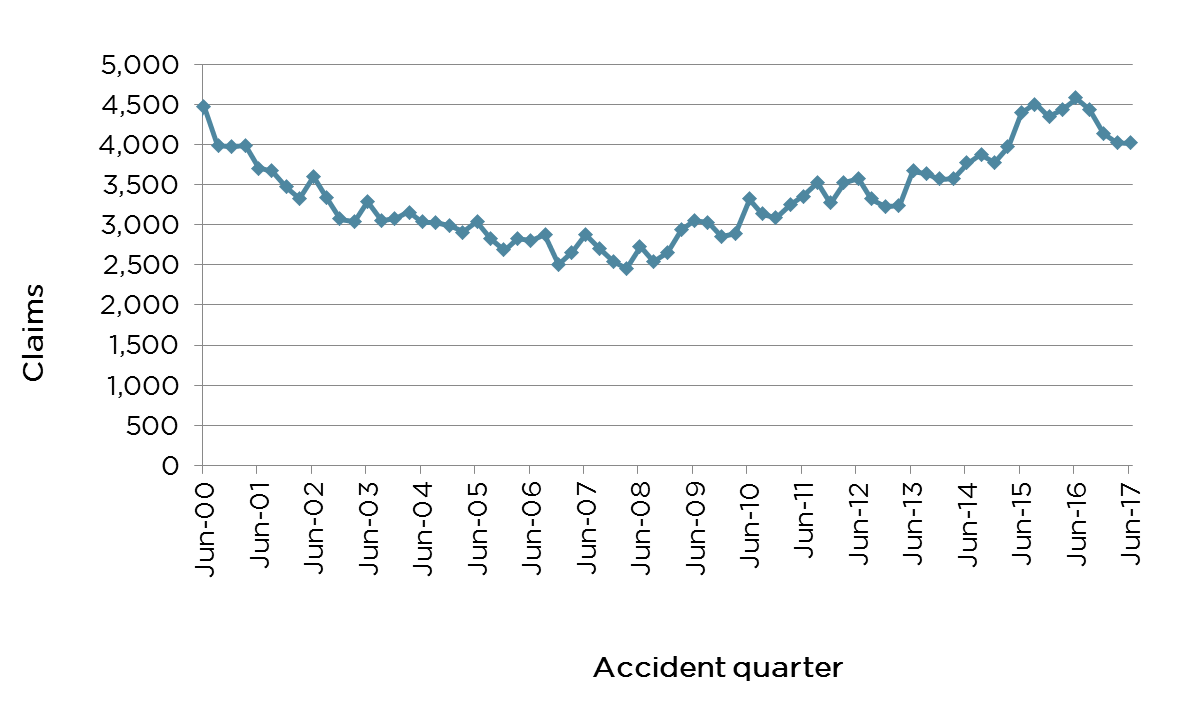

Claims by accident quarter

Graph 4: Claims by accident quarter

Graph 4 shows the number of CTP claims per accident quarter[2]. Since March 2008 there has been a clear upward trend in the number of claims per accident quarter from 2,451 in March 2008 to 4,597 in June 2016 and thereafter the number of CTP claims per accident quarter is estimated to decline to 4,020 in March 2017 and 4,016 in June 2017.

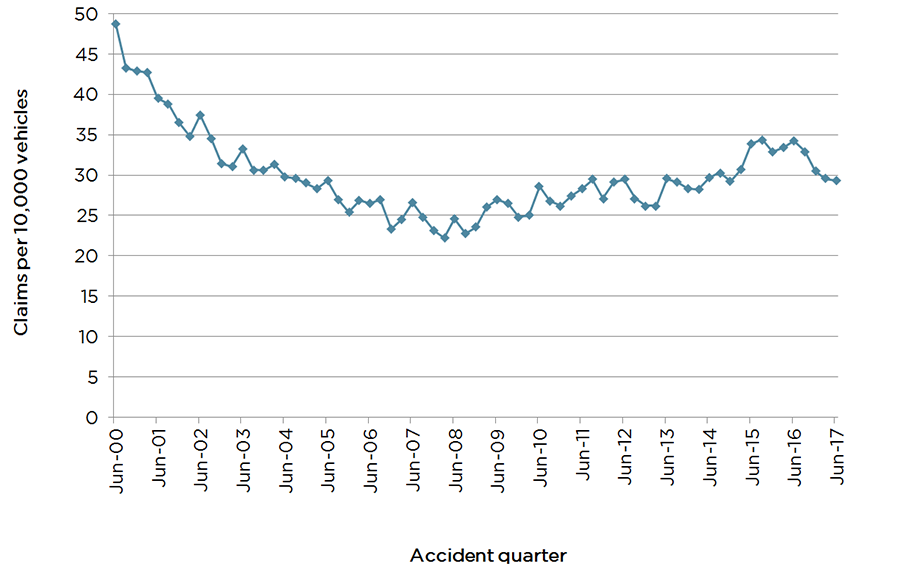

Claim frequency

Graph 5: Trend in claims frequency

Note: For the more recent accident quarters, projections are based on incomplete claims hence data presented for these quarters are just indicative and depend on the robustness of ultimate claims projections.

Claim frequency is defined as the ultimate number of claims divided by the number of registered vehicles. The ultimate number of claims comprises all reported notifications (full claims and Accident Notification Forms (ANFs)) plus an estimate of claims yet to be reported.

Graph 5 shows the trend in claim frequency by accident quarter. Claims frequency increased consistently from 22 claims per 10,000 vehicles in March 2008 to 34 claims per 10,000 vehicles in June 2016 and thereafter it has declined. The estimated claim frequency for the June 2017 accident quarter is 29 claims per 10,000 vehicles and the average for the year to June 2017 is 31 claims per 10,000 vehicles.

Claims cost

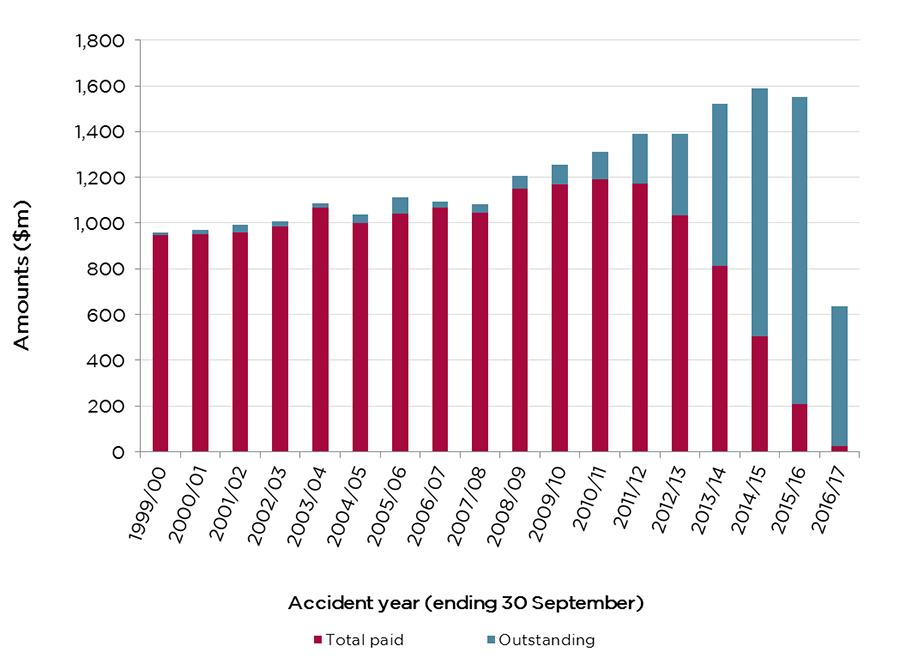

Graph 6: Payments on reported claims as at 30 June 2017

As at 30 June 2017, a total of 237,366 notifications (full claims and ANFs) with a total incurred cost of $21.18 billion[3] has been reported since the current scheme commenced in October 1999. It is estimated that $4.9 billion (23%) is yet to be paid for claims reported to date.

Graph 6 shows how this unpaid amount is distributed across prior full accident years. Further development in payments has been happening for accident year 2016/17, which has three out of four quarters worth of claims reported for the accident year as at 30 June 2017. Also, as late claims are reported and estimates for already reported claims get revised, the actual incurred cost becomes more evident.

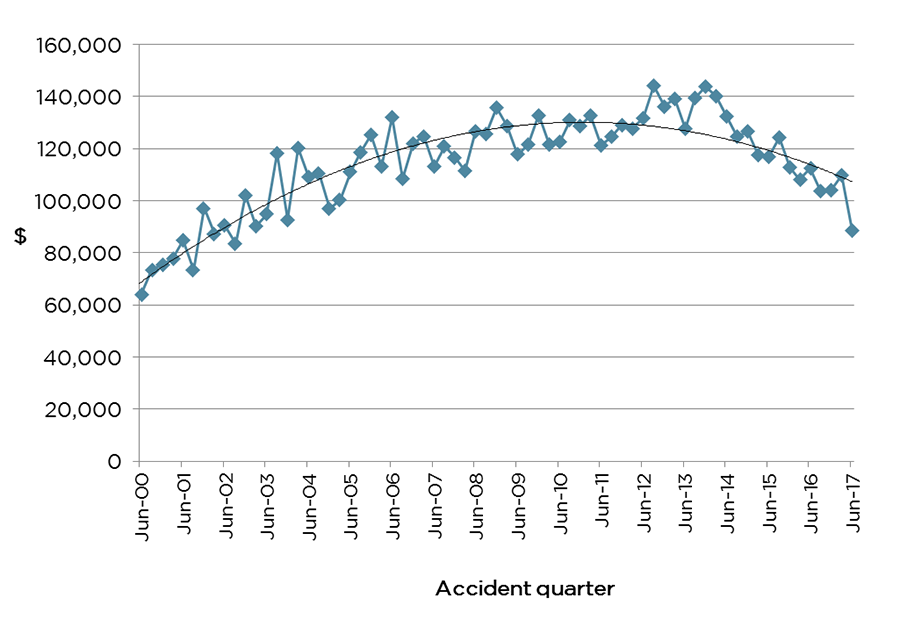

Graph 7: Average incurred cost (full claims only)

The trend in average incurred costs of full claims[4] that have already been lodged with CTP insurers is shown in Graph 7. The incurred costs are historic amounts supplied by insurers and are not adjusted for inflation.

Since the start of the MACA 1999 scheme, the average incurred cost increased from about $68,000 in March 2000 to about $145,000 in September 2012 and then began to fall thereafter. For claims already reported, insurers will continue to revise their cost estimates as more information is received on these claims. Insurers are yet to receive late claims from some accidents that have already occurred but not yet had claims lodged; this especially applies to the four most recent accident quarters.

These revisions and late reports introduce some uncertainty in the average cost estimates hence the trend line superimposed on Graph 7 presents a more likely level of final average costs of claims in more recent accident quarters. The average incurred costs of claims, arising from accidents in the June 2016 quarter is more likely to be around $115,000 and $109,000 for claims from the June 2017 quarter.

About SIRA

SIRA is the government organisation responsible for the regulation of workers compensation insurance, motor accidents compulsory third party (CTP) insurance and home building compensation in NSW.

We focus on ensuring key public policy outcomes are achieved in relation to service delivery to injured people, affordability, and the effective management and sustainability of these insurance schemes.

For the NSW motor accidents insurance scheme, we monitor insurer performance, support road safety initiatives, promote optimal recovery for injured people and provide an independent dispute resolution service.

SIRA assumed the regulatory functions of the former Motor Accidents Authority from 1 September 2015.

Contact

Director, CTP Market & Premium Supervision

SIRA – Motor Accidents Insurance Regulation

[email protected]

Notes

1. Operation Strike Force Ravens, funded by SIRA and run by the Fraud & Cybercrime Squad of NSW Police in August 2016.

2. The numbers of claims reported for accidents from 2014 onward, includes projections for claims incurred but not yet reported (IBNR).

3. Incurred cost comprises the amount already paid on claims plus an estimate for likely future payments on claims yet to be finalised. Incurred costs shown here are as reported by insurers and have not been adjusted for inflation.

4. Full claims account for over 99% of scheme incurred claims costs