Print PDF

Green Slip scheme quarterly insights - March 2018

Download the PDF (3,898KB)

Executive Director’s message

This was our first full quarter with the new 2017 Green Slip scheme in operation.

I am pleased to report insurers and State Insurance Regulatory Authority (SIRA) have quickly adapted to the new scheme’s focus: the optimal recovery of injured people and timely financial support for those who are earners.

Our multi-channel support and information service, CTP Assist, has been busy connecting injured people to the correct insurer and helping them lodge and manage their claim. Through regular supervision visits, our Claims and Customer Outcomes team have seen proactive practices by insurers to give injured people early support. We’re continuing to develop training and guidance resources to further reinforce high standards in insurer claims handling.

For the policy holder, average premium prices remain low for motor vehicles compared to November prices under the old 1999 scheme. Premium refunds are available for those who paid pre-reform prices for Green Slips starting before 1 December 2017.

Apart from regulating the Green Slip scheme, we have a legislated responsibility to invest in road safety research. This quarter, SIRA, in conjunction with the Centre for Road Safety, Transport for NSW, has been developing a statewide in-vehicle telematics road safety pilot. The aim is to reduce casualties by improving young driver behaviour. The pilot will provide an understanding of how telematics-driven feedback can help moderate risky driving behaviours in high-risk young drivers.

In all, we’re running to plan. We continue to closely monitor the scheme, and fine tune our support services and insurer supervision practices, to deliver better outcomes for the road users of NSW – especially those injured in motor vehicle accidents.

State Insurance Regulatory Authority (SIRA)

The scheme to date

Some key figures for the 2017 CTP scheme for its first four months: 1 December 2017 to 31 March 2018.

- Over 1 million Green Slip checks

- 16,060 people helped by CTP Assist

- 2,181 claims lodged

- Average premium $509, 18% down (NSW average passenger vehicle premium March 2018 vs March 2017)

- Payments $5,577,520 for treatment expenses, weekly payments, care, funeral expenses, insurer costs

- $62.5 million refunded

Young drivers telematics pilot:

making our roads safer

We are developing a statewide in-vehicle telematics road safety pilot, in partnership with the Centre for Road Safety, Transport for NSW. The aim is to reduce casualties on NSW roads by improving driver behaviour.

Young drivers are among the highest-risk groups on the road: up to five times more likely to be involved in crashes resulting in serious injury or death according to Centre for Road Safety data.

The pilot will help us understand how telematics-driven feedback can help moderate risky driving behaviours in high-risk young drivers.

We’re recruiting 1,000 young drivers from across NSW, focused on Western Sydney and regional areas – higher-risk parts of the state. Each will have a telematics system installed in their car. This will track a range of driving parameters, for example: hard braking and acceleration, cornering forces, distances travelled and time of day.

Tight rules will be in place to protect drivers’ privacy. All identifying data will be removed before analysis.

The pilot will start in the second half of 2018 and drivers who participate will each be paid $100.

To find out more or sign up for the trial, head to the telematics page on SIRA's website.

Green Slip Check

The new Green Slip Check has been available for five months, saving motorists time when shopping around for the best deal on a Green Slip.

It’s a fast, user-friendly, comparison tool which will also help us improve our services for motorists. Better data collection with the new tool also supports our regulatory role and encourages competition among insurers.

People who entered vehicle information to the Green Slip Check

| January 2018 | 253,988 |

| February 2018 | 250,325 |

| March 2018 | 338,833 |

Green Slip refunds

$62.5 million in Green Slip refunds was returned to vehicle owners, businesses and taxis this quarter, as part of the NSW Government’s reforms.

Six-month policies may also be eligible for the refund if they started towards the end of 2017.

All surplus and unclaimed funds will be returned to motorists through a reduction in the SIRA Fund levy next year.

Green Slip prices were reduced for most classes of vehicles1 from 1 December 2017 when the new scheme started. So, if people bought or renewed a Green Slip with a start date before 1 December, they may have paid pre-reform prices.

The refund applies to the owner of the vehicle as at midnight 30 November 2017 and is calculated proportionally. That is, the closer the policy start is to 1 December 2017, the larger the refund.

An advertising campaign has been running across NSW to encourage people to claim online via Service NSW.

Note 1: Motorcycle owners will not receive a refund. Instead, injured motorcycle riders, particularly those at fault in the accident, will get more benefits under the new scheme.

1999 and 2017 schemes

Insurers sold their last policies under the 1999 scheme on 30 November 2017 and started selling policies under the 2017 scheme on 1 December 2017.

The 1999 scheme will continue operating for several years until licensed insurers finalise claims for accidents that happened before 1 December.

Consequently, SIRA is regulating two schemes for a period: the 2017 scheme and claims under the 1999 scheme that aren’t yet finalised.

CTP Assist: help for the injured and their families

CTP Assist is our multi-channel support service, providing personalised claims support and information for injured people and other participants in the CTP scheme such as doctors and health professionals. Our consultants routinely phone injured people after they have lodged a claim, to make sure they are getting the support they need. The same consultant calls each time to maintain a strong connection with each claimant.

For the three months to 31 March 2018, the CTP Assist team handled the following contacts with injured people in both schemes:

13,285 injured people helped by phone and digital channel

795 injured people connected with an insurer

8,797 calls made to ensure injured people were getting the treatment and support they needed

Here are some examples of people recently helped (please note names and personal details have been changed for privacy).

Helping a vulnerable person get the financial support he needs

Josh’s parents were overseas and he found himself with no money because he could not work as a result of an accident. While he’d lodged a CTP claim, the insurer wouldn’t accept it because Josh was under 18.

Our CTP Assist consultant contacted the insurer, who confirmed this. After our consultant escalated the issue and explained the situation, the insurer accepted Josh’s claim and began benefit payments immediately.

Sometimes facts slip through the cracks

An insurer refused to backpay weekly benefits to Stefan, saying he hadn’t lodged the claim within the required 28 days.

The accident had involved four cars, and fault hadn’t been established straight away. The claim had originally been lodged with the wrong insurer – something Stefan’s insurer hadn’t picked up on. Once our CTP Assist consultant filled them in, they accepted the claim and agreed to backdate his payments.

Help with getting back to work

Regular follow-up calls are part of the service

Susan was recovering slowly from a lower back injury and was still quite restricted in her movements. Her insurer had accepted liability for the first 26 weeks after the accident.

Although she was keen to return to work, Susan’s employer had said there were no suitable duties. Her daughter had called CTP Assist as she was concerned her mother would lose her job.

CTP Assist encouraged them to have their insurer discuss options with the employer. The result? By 10 weeks, Susan was back at work full-time on suitable duties, after the insurer and employer had arranged this. She’s much happier and is steadily recovering from her injury under her doctor’s supervision.

Getting everyone talking

CTP Assist received a call from Rohan, who was very unhappy with the way his managing insurer had calculated his weekly benefit, the time taken to approve the multiple treatments he needed and their response to his concerns.

Our consultant contacted the insurer and, while there are still some matters in dispute, Rohan was very pleased with SIRA’s help and has now been able to engage effectively with the insurer.

Getting a doctor on side

During the CTP Assist consultant’s regular three week follow-up call, Andrew told us his surgeon wouldn’t deal with insurers and said he’d have to pay directly for treatment and get reimbursed.

Our consultant called the insurer’s case manager and said we didn’t want any injured people out of pocket for their treatment. We suggested they contact the doctor and see if they could persuade him to work with them, or to see if Andrew was willing to see another doctor.

The insurer’s case manager contacted the surgeon and addressed his concerns, so he agreed to work directly with the insurer, making Andrew much happier.

CTP Legal Advisory Service

A CTP Legal Advisory Service pilot was launched by SIRA in mid-December 2017. The service provides legal phone advice relating to statutory benefits claims, where legal fees are restricted by the Motor Accidents Injuries Act 2017 and supporting Regulation.

To use the service, an injured person can simply call CTP Assist who will help arrange a referral if they are eligible. Advice is personal and confidential. There is no charge to injured people.

Key statistics 2017 scheme

This report focuses on the three months from 1 January to 31 March 2018, with some data from the scheme’s commencement on 1 December 2017. Further analysis will be provided as the scheme progresses. Insurers have 28 days after an accident to determine a claim for benefits for the first 26 weeks. They must determine liability beyond 26 weeks within three months of the accident.

While it is too early for trends to be visible, we are closely monitoring the scheme.

Claims

1 January to 31 March 2018

| Early notifications (38%) | 97 |

| Full claims (62%) With legal representation | 324 1,730 |

| Claims lodged where fault is not yet determined | 1,251 |

| Not at fault claims lodged | 667 |

| At fault claim lodged | 136 |

| Total number of claims lodged | 2,054 |

Injury types

| Soft tissue injuries (including neck and back strain) | 538 |

Claims by gender

| Male | 1,015 |

| Female | 1,036 |

| X | 3 |

Disputes

1 December 2017 to 30 June 2018

| Internal insurer reviews | 315 |

| Valid disputes lodged with Dispute Resolution Service (DRS) | 68 |

Payments

1 December 2017 to 31 March 2018

| Payment type | Amount |

|---|---|

| Weekly payments | 2,954,786 |

| Treatment expenses | 1,921,928 |

| Care | 174,573 |

| Funeral expenses | 388,316 |

| Insurer investigations | 135,213 |

| Insurer medico-legal | 2,704 |

| Insurer legal | 0 |

| Claimant costs (excluding legal) | 0 |

| Claimant legal | 0 |

| Total | 5,577,520 |

Claim by age

| Age group | No. of claims | % of total by age |

|---|---|---|

| 0-16 years | 84 | 4% |

| 17-24 years | 239 | 12% |

| 25-39 years | 625 | 30% |

| 40-49 years | 385 | 19% |

| 50-64 years | 450 | 22% |

| 65-79 years | 214 | 10% |

| 80+ years | 57 | 3% |

| Total | 2,054 | 100% |

Claims by insurer

| Insurer | No. of claims | % of total by insurer |

|---|---|---|

| AAMI | 183 | 9% |

| Allianz | 233 | 11% |

| CIC Allianz | 102 | 5% |

| GIO | 532 | 26% |

| NRMA | 636 | 31% |

| QBE | 368 | 18% |

| Total | 2,054 | 100% |

Claims by occupation

| Occupation | No of claims | % of total by occupation |

|---|---|---|

| Clerical and administrative workers | 57 | 3% |

| Community and personal service workers | 35 | 2% |

| Labourers | 149 | 7% |

| Machine operators and drivers | 32 | 2% |

| Managers | 53 | 3% |

| Professionals | 98 | 5% |

| Sales workers | 30 | 1% |

| Technicians and trades workers | 51 | 2% |

| Non-earners2 | 333 | 16% |

| Yet to be advised3 | 1,216 | 59% |

| Total | 127 | 100% |

Note 2: This also includes children, retirees and those not working

Note 3: It can take up to four weeks to determine occupation

Claims for damages: future economic loss and pain and suffering

In the 2017 scheme, damages claims may be made by people who have an injury that is not a minor injury and were not at fault in the accident. If they’re partially at fault, damages may be reduced. At the time of this report, no valid damages claims for future earnings and pain and suffering had been received.

During the first 20 months after an accident, the person receives lost income, treatment, care and rehabilitation, to promote optimal recovery. After 20 months, those with injuries other than minor injuries may submit a damages claim.

People seriously injured in a motor vehicle accident can make a damages claim immediately after the accident. Seriously injured people are people with injuries that result in a greater than 10 per cent whole person impairment.

Future medical costs don’t need to be claimed, as medical treatment and care are provided under statutory benefits (personal injury benefits). For people with injuries that are not minor injuries, these are available for life if necessary.

If an accident is fatal, the deceased person’s family can make a claim for funeral expenses, which are paid automatically, regardless of who was at fault in the accident.

Scheme insurers

The Green Slip market is privately underwritten4 by six licensed insurers operated by four organisations: Suncorp (AAMI and GIO), Allianz Australia (Allianz and CIC Allianz), NRMA and QBE. Zurich stopped issuing Green Slip policies to the public on 1 March 2016 under the 1999 scheme.

Note 4: Underwriting describes the process of assessing risk and ensuring the cost and conditions of the cover are proportionate to the risks faced by the individual concerned.

Below is a comparison of current Sydney best prices for passenger motor vehicles with prices at the start of the 2017 scheme on 1 December 2017. Prices are for drivers aged 30 to 54.

Best prices by insurer

| Insurer | 1 Dec 2017 | March 2018 | Best price change |

|---|---|---|---|

| NRMA | $468 | $468 | 0% |

| GIO | $475 | $475 | 0% |

| AAMI | $475 | $475 | 0% |

| Allianz | $488 | $478 | -2% |

| QBE | $470 | $470 | 0% |

| CIC Allianz | $454 | $454 | +3% |

Premiums

Allianz and CIC Allianz introduced new premiums from 7 February 2018. Allianz reduced their best price for a Sydney passenger vehicle by $10, from $488 to $478. CIC Allianz increased their best price for a Sydney passenger vehicle by $13, from $454 to $467. CIC Allianz remains the best price market leader, however it deals predominantly in fleet vehicles in the non-retail sector.

GIO submitted a filing5 to start from 25 May 2018 which was accepted by SIRA.

Note 5: A filing shows proof of financial responsibility in setting premiums.

Market share

The graph below shows the proportion of premiums collected by insurers from the March 2017 quarter to the March 2018 quarter and includes the 2017 scheme. This graph is based on a rolling 12-month period and shows smoother trends in market share as it compensates for seasonal renewals of large fleets of vehicles.

During this quarter, NRMA retained the largest market share with 31%, followed by QBE with 24.1% and GIO with 17.9%.

Premium market share (rolling 12-month) comparison

on premiums paid by motorists without adjustment for any refunds as a result of the new scheme. Independent analysis showed the impact of including the refunds was minimal on each insurer’s market share. All insurers agreed with this approach.

trends

The graph below shows the average premium trends over the past five years for passenger vehicles in Sydney metropolitan and country regions.

The average premium paid by all NSW passenger vehicle owners for their Green Slip was $509, a $118 (18.8%) reduction compared to the March 2017 quarter figure of $627. The reduction is principally due to the reforms and partly due to reductions in claim frequency in recent quarters. NSW Police’s Strike Force Ravens counter fraud activities have contributed to this reduction.

Average premium trends over the last five years (includes GST and levies)

Insurer supervision

As a risk-based regulator, we assess risks to the performance of the scheme and choose appropriate interventions to achieve the best overall outcomes.

Our Claims and Customer Outcomes team, through regular supervision visits to insurers, focuses on providing advice and education to encourage sound claims management practices. We’re developing training and guidance resources to reinforce high standards in insurer claims handling.

During our first review, just a few weeks into the 2017 scheme, we found some inconsistency in screening and minimal delays in establishing access to statutory benefits. Working with the insurers, we helped clarify what was required and found things much improved in our March review.

An example of this is risk screening, the first step for an insurer once a claim is lodged. After four months’ experience with the new scheme, insurers seem comfortable with the process, usually completing it within three days, applying statutory benefits and effectively using evidence to make consistent, accurate decisions.

Insurer internal reviews

30 insurer internal reviews were lodged in this quarter.

This must be independent of the original decision maker, allowing the injured person and insurer to resolve the dispute without needing SIRA’s Dispute Resolution Service (DRS). This will reduce the number of disputes that DRS must consider and should provide a quicker outcome for injured people.

An insurer internal review is needed before most disputes can be lodged with DRS.

Internal reviews by decision type

| Amount of weekly benefit payments | 7 |

| Is the death or injury from an accident in NSW? | 2 |

| Is the injured person mostly at fault? | 1 |

| Is the injury more than a minor injury? | 4 |

| No benefits if workers compensation payable | 1 |

| Reduction for contributory negligence | 1 |

| Is treatment and care reasonable and necessary? | 14 |

| Total | 30 |

Internal reviews by outcome

| All treatment allowed - better for claimant | 3 |

| Claim may be made | 1 |

| Claim may not be made | 1 |

| Original decision confirmed | 4 |

| Original decision overturned - better for claimant | 1 |

| Original decision overturned - worse for claimant | 0 |

| No treatment allowed - same outcome for claimant | 7 |

| No treatment allowed - worse for claimant | 1 |

| Same outcome for claimant | 0 |

| Review withdrawn | 1 |

| Reviews in progress at 31 March 2018 | 11 |

| Total | 30 |

Dispute Resolution Services

"The Dispute Resolution Service is absolutely focused on the best services and outcomes for injured road users. Resolving disputes as quickly, as fairly and as economically as possible without compromising on the time and care needed to fully address their concerns."

Cameron Player, Executive Director, Dispute Resolution Services division, SIRA.

SIRA’s Dispute Resolution Services division provides an alternative to court for resolving disputes in the NSW workers compensation system, the NSW compulsory third party scheme and the Lifetime Care and Support schemes in NSW and the ACT.

For people injured in motor accidents and insurers, it provides a fast, cost-effective and fair way to resolve disputes. The service is delivered without charge to injured people and insurers. It is provided through the Fund levy, a component of Green Slip premiums

Personal service and support at every step

Our DRS concierge team is ready to help injured road users, insurers and legal representatives access any of our services, through our new online portal, by email, phone or in person.

If a dispute does need to be referred to DRS, a single application form is all that’s needed. A dispute resolution officer (DRO) is assigned, so injured people only have to deal with one person about any of the disputes they may have. DROs identify, clarify and seek to narrow issues in dispute to help the parties reach a resolution early. Where necessary, they can also allocate disputes to independent decision-makers for determination, including DRS Merit Reviewers, DRS Medical Assessors or one of the DRS Claims Assessors, led by the Principal Claims Assessor.

Keeping the scheme sustainable

Fraudulent claims, with staged accidents, exaggerated injuries and collusion, are a burden for motor accident insurance schemes around the world.

The cost of this is carried by the whole community, specifically in the premiums we pay for our insurance. So reducing fraud benefits everyone.

New laws have strengthened SIRA’s ability to investigate and prosecute people attempting to cheat the system.

Update from Strike Force Ravens

We continue to work with the NSW Police’s Strike Force Ravens to deter, detect and prosecute fraudulent claims.

There were no arrests made or charges laid during the March 2018 quarter.

Key statistics 1999 scheme

While the last 1999 scheme CTP policies were sold on 30 November 2017, people injured up to that date can submit a claim for up to six months after the accident.

Any disputes that may arise in those claims in the months and years ahead may still be referred to the Medical Assessment Service (MAS) and the Claims Assessment and Resolution Service (CARS) which continue to operate. Consequently, this scheme will be in operation for many years, as people’s injuries, claims and any disputes which may arise are resolved

Claims (all data as at 31 March 2018)

| New claims lodged in this reporting period | 1,000 |

| Not-at-fault Accident Notification Form (ANF) | 6 |

| At fault ANF | 27 |

| Full claim direct | 941 |

| Full claim converted from an ANF | 26 |

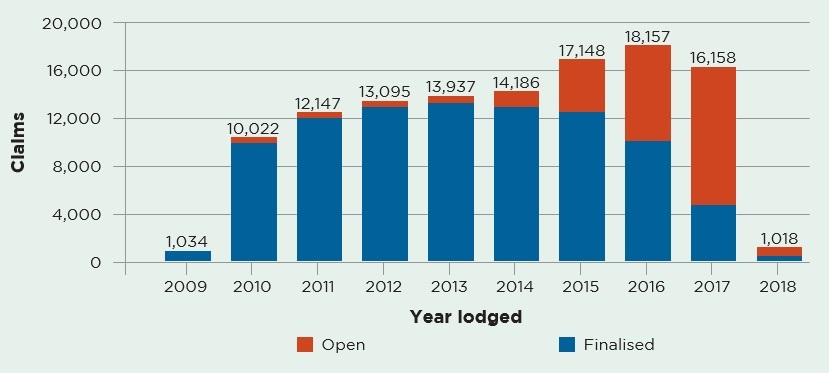

Open and closed claims by lodgement year

Open or active claims

As of 31 March 2018, there were 27,630 open claims under the 1999 scheme. This compares with 28,967 as at 31 December 2017.

The time to settle a claim may be affected by the time it takes for an injury to stabilise, enabling the parties to assess whether there may be an entitlement to non-economic loss damages, and to resolve any disputes. It is not uncommon for claims to take three to five years to be resolved.

As people injured up to 30 November 2018 have up to six months after their accident to submit a claim, lodgement of claims will cease on 30 June 2018, with the exception of a few late claims that may be accepted by the courts.

March 2018:

$290m total gross paid in March quarter

$4.8b outstanding estimate by insurers as at 31 March 2018

Total claims by insurer

| Insurer | No of claims | % of total by insurer |

|---|---|---|

| Zurich | 2 | 1% |

| AAMI | 104 | 10% |

| Allianz | 99 | 10% |

| CIC Allianz | 63 | 6% |

| GIO | 199 | 20% |

| NRMA | 299 | 30% |

| QBE | 234 | 23% |

| Total | 1,000 | 100% |

Injured people with legal representation

| Total new claims | |

|---|---|

| Self-represented | 316 |

| Legally represented | 684 |

| Total | 1,000 |

Medical Assessment Service

SIRA’s Dispute Resolution Services division also delivers the Motor Accidents Medical Assessment Service (MAS), as part of the 1999 scheme, to resolve any medical disputes between injured people and insurers.

Medical disputes are referred to independent expert decision-makers (MAS Medical Assessors) for determination.

Medical assessments, particularly about permanent impairment, are usually referred to MAS about two and a half years after a motor accident, once injuries have stabilised. So we expect to see the volume of disputes continuing at the current rate until about mid-2020, for accidents occurring before the new scheme started on 1 December 2017

New medical disputes referred to MAS

| Permanent impairment | 909 |

| Treatment and care | 127 |

| Further medical assessment | 72 |

| Medical assessment review | 231 |

| Total for quarter ended 31 March 2018 | 1,339 |

| Total for previous quarter | 1,407 |

Disputes resolved by MAS

There were 1,280 disputes resolved by MAS this quarter, compared with 1,458 in the previous quarter.

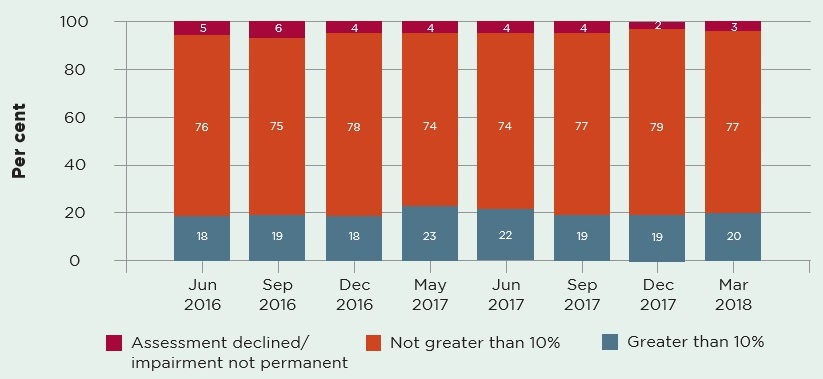

The predominant medical disputes determined by independent MAS Medical Assessors are disputes about permanent impairment, to help parties determine whether an injured person is entitled to claim damages for non-economic loss.

Injured people who have been assessed with permanent impairment of greater than 10% may claim for damages.

Over 900 permanent impairment disputes were resolved in the March quarter. As the graph below shows, 20% of these were assessed as having a greater-than-10% permanent impairment, which is consistent with prior periods.

MAS permanent impairment disputes – assessed outcomes by type

Claims Assessment and Resolution Service

Dispute Resolution Services also deliver the Motor Accidents Claims Assessment and Resolution Service (CARS), as part of the 1999 scheme, to resolve any claims disputes between people injured in motor accidents and insurers.

Claims disputes are referred to independent expert decision-makers (CARS Claims Assessors), led by the Principal Claims Assessor.

Claims assessments are usually referred to CARS about three years after a motor vehicle accident, once injuries have stabilised and any damages can be assessed and potentially negotiated by the parties. So we expect to see the volume of claims assessments referred to CARS continuing at the current rate until about 2020, three years after the new scheme commenced.

New claims disputes referred to CARS

| General claims assessment | 437 |

| Further general claims assessment | 0 |

| Special assessments of procedural disputes | 34 |

| Applications for exemption from claims assessment | 537 |

| Total for quarter ended 31 March 2018 | 1,028 |

| Total for previous quarter | 949 |

Disputes resolved by CARS

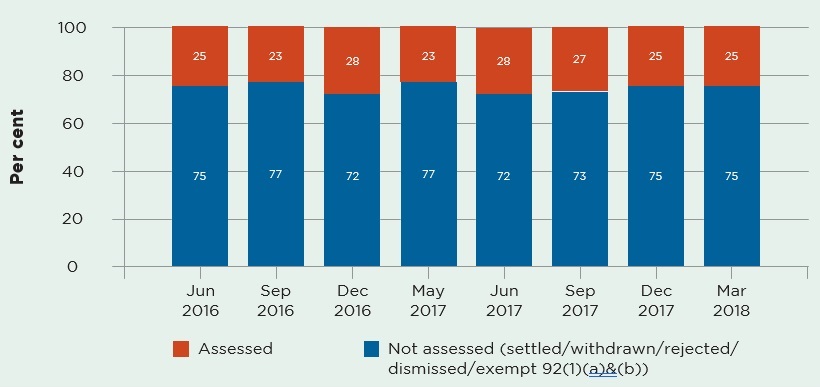

This quarter 925 disputes were resolved by CARS, compared with 979 disputes resolved in the previous quarter.

General assessments of claims are the predominant dispute referred to CARS. These may include assessments of liability, damages and legal costs. Over 400 were resolved in the March quarter, most without the need for a decision by a CARS Claims Assessor.

CARS claims assessments disputes resolved (with and without an assessment)

Administrative law challenges to decisions

Decisions made by statutory administrative decision-makers, including Merit Reviewers, Medical Assessors and Claims Assessors, are all potentially subject to administrative law judicial review in the NSW Supreme Court.

During this quarter there were over 2,000 disputes resolved by MAS and CARS, and none, as yet, by DRS in the new CTP scheme.

Administrative challenges involving each of these services this quarter included:

CARS

Two challenges to CARS decisions were commenced, both on behalf of an insurer.

No challenges to CARS Claims Assessors decisions were determined by the courts.

Seven challenges to CARS Claims Assessors’ decisions are currently before the courts.

MAS

Eight challenges to MAS decisions were commenced, six on behalf of an injured person and two on behalf of an insurer.

Four challenges to MAS Medical Assessors’ decisions were finalised by the courts:

- one decision was upheld

- three decisions were set aside and returned to MAS for a fresh decision.

Twelve challenges to MAS Medical Assessors’ decisions are currently before the courts.

Complaints and compliments

MAIR will be reporting regularly on complaints and compliments under the 2017 scheme. Complaints will be used to improve service delivery and identify any unwelcome trends emerging in the scheme.

Reviews by the Compliance, Enforcement and Investigations team

There were 31 complaints made against insurers under the 1999 scheme during the quarter. These were either reviewed, or are still under review, by SIRA’s Compliance, Enforcement and Investigations team.

Of the 31 complaints, 20 have been resolved:

- 12 in favour of the claimant

- five in favour of the insurer

- three were dismissed and resolved in neither party’s favour.

Complaint reasons:

- 11 alleged breaches of the Claims Handling Guidelines

- seven alleged breaches of the treatment rehabilitation and care (TRAC) guidelines

- eight related to inappropriate insurer behaviour or conduct

- five alleged the insurer was not just and expeditious in resolving a claim.

Letters to the Minister

There were 57 letters to the Minister for Finance, and Services and Property during the quarter.

Letters to the Minister by topic

| Topic | Representations |

|---|---|

| Prices | 14 |

| Claims | 5 |

| Refunds | 7 |

| Levy | 4 |

| Premium rating factors | 5 |

| Mobility scooters | 2 |

| Point to point transport | 6 |

| Motor vehicle registration | 4 |

| Other | 10 |

| Total | 57 |

Conclusion

MAIR will continue to monitor scheme performance closely. And, as scheme milestones are reached, we’ll be providing a more comprehensive picture of the injured person’s journey.

We expect our first disputes to be determined by SIRA’s Dispute Resolution Service in the next quarter as, at three months after an accident, insurers must determine whether benefits beyond 26 weeks are payable. This quarter, injured people have resolved disagreements with their insurers using the independent insurer internal review process that’s part of the new system.

Positive customer experiences are important to us and we will continue to report on feedback that CTP Assist receives while helping injured people.

The remaining claims in the 1999 scheme will be monitored and we will make sure all injured people are dealt with fairly throughout the claims process.

Feedback on how we can improve this report is appreciated and can be sent to: [email protected].